import pandas as pd

from sklearn.datasets import fetch_california_housing

from sklearn.model_selection import train_test_split

housing = fetch_california_housing(as_frame=True)

X = housing.data

y = housing.target.rename("MedHouseVal")

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.2, random_state=42

)Tutorial: Probabilistic Regression

Full predictive distributions with the skpro interface

The partition_tree.skpro module exposes the same Partition Tree algorithm through the skpro BaseProbaRegressor interface. Instead of a scalar prediction, predict_proba returns an IntervalDistribution — a piecewise-constant density that you can query for PDF values, CDFs, quantiles, prediction intervals, and random samples.

NoteJust want point predictions?

See the Regression tutorial, which uses the lighter-weight partition_tree.sklearn interface and returns plain NumPy arrays.

Setup

1. Baseline — Decision Tree (CART)

CART produces only point predictions, so we use MAE and R² as the comparison baseline.

from sklearn.tree import DecisionTreeRegressor

from sklearn.metrics import root_mean_squared_error, r2_score

import numpy as np

cart = DecisionTreeRegressor(random_state=42)

cart.fit(X_train, y_train)

y_pred_cart = cart.predict(X_test)

print("=== DecisionTreeRegressor (CART) ===")

print(f"RMSE : {root_mean_squared_error(y_test, y_pred_cart):.4f}")

print(f"R² : {r2_score(y_test, y_pred_cart):.4f}")

print("(no probabilistic output available)")=== DecisionTreeRegressor (CART) ===

RMSE : 0.7037

R² : 0.6221

(no probabilistic output available)2. Single Partition Tree

Fit and point prediction

from partition_tree.skpro import PartitionTreeRegressor

pt = PartitionTreeRegressor(

min_volume_fraction=0.1,

)

pt.fit(X_train, y_train)

# Point prediction — posterior mean of the conditional density

y_pred_pt = pt.predict(X_test)print("=== PartitionTreeRegressor ===")

print(f"RMSE : {root_mean_squared_error(y_test, y_pred_pt):.4f}")

print(f"R² : {r2_score(y_test, y_pred_pt):.4f}")=== PartitionTreeRegressor ===

RMSE : 0.5879

R² : 0.7362Comparison with CART

pd.DataFrame({

"Model": ["DecisionTree (CART)", "PartitionTree"],

"RMSE": [

root_mean_squared_error(y_test, y_pred_cart),

root_mean_squared_error(y_test, y_pred_pt),

],

"R²": [

r2_score(y_test, y_pred_cart),

r2_score(y_test, y_pred_pt),

],

}).round(4)| Model | RMSE | R² | |

|---|---|---|---|

| 0 | DecisionTree (CART) | 0.7037 | 0.6221 |

| 1 | PartitionTree | 0.5879 | 0.7362 |

Probabilistic prediction

predict_proba returns an IntervalDistribution:

dist = pt.predict_proba(X_test)

print(type(dist))<class 'partition_tree.skpro.distribution.IntervalDistribution'>3. The IntervalDistribution API

From the distribution object you can extract:

# Posterior mean (same as predict)

mean = dist.mean()

# Posterior variance

var = dist.var()

# Quantiles via the inverse CDF (percent-point function)

median = dist.ppf(0.5)

lower_90 = dist.ppf(0.05)

upper_90 = dist.ppf(0.95)

# Random samples from the predictive distribution

samples = dist.sample(n_samples=100)

# PDF / CDF evaluated at specific points

pdf_vals = dist.pdf(y_test.to_frame())

cdf_vals = dist.cdf(y_test.to_frame())

print("mean shape :", mean.shape)

print("var shape :", var.shape)

print("ppf shape :", median.shape)mean shape : (4128, 1)

var shape : (4128, 1)

ppf shape : (4128, 1)| Method | Returns |

|---|---|

mean() |

Posterior mean — pd.DataFrame |

var() |

Posterior variance — pd.DataFrame |

pdf(x) |

Density at x — pd.DataFrame |

log_pdf(x) |

Log-density at x — pd.DataFrame |

cdf(x) |

CDF at x — pd.DataFrame |

ppf(q) |

Quantile at level q — pd.DataFrame |

sample(n_samples) |

Random samples — pd.DataFrame |

energy(x) |

Energy score — pd.DataFrame |

plot(ax) |

Plot the piecewise-constant PDF |

4. Prediction Intervals

Prediction intervals are constructed directly from the inverse CDF.

import numpy as np

# 80 % prediction interval: [10th percentile, 90th percentile]

lower_80 = dist.ppf(0.10)["MedHouseVal"]

upper_80 = dist.ppf(0.90)["MedHouseVal"]

y_true = y_test.values

covered = ((y_true >= lower_80.values) & (y_true <= upper_80.values)).mean()

print(f"80% PI empirical coverage: {covered:.1%}")80% PI empirical coverage: 76.1%

NoteWhy coverage may differ from the nominal level

The Partition Tree density is learned from training data, so calibration improves with more data and better-tuned hyperparameters. Using PartitionForestRegressor (Section 5) typically yields better-calibrated intervals through density averaging.

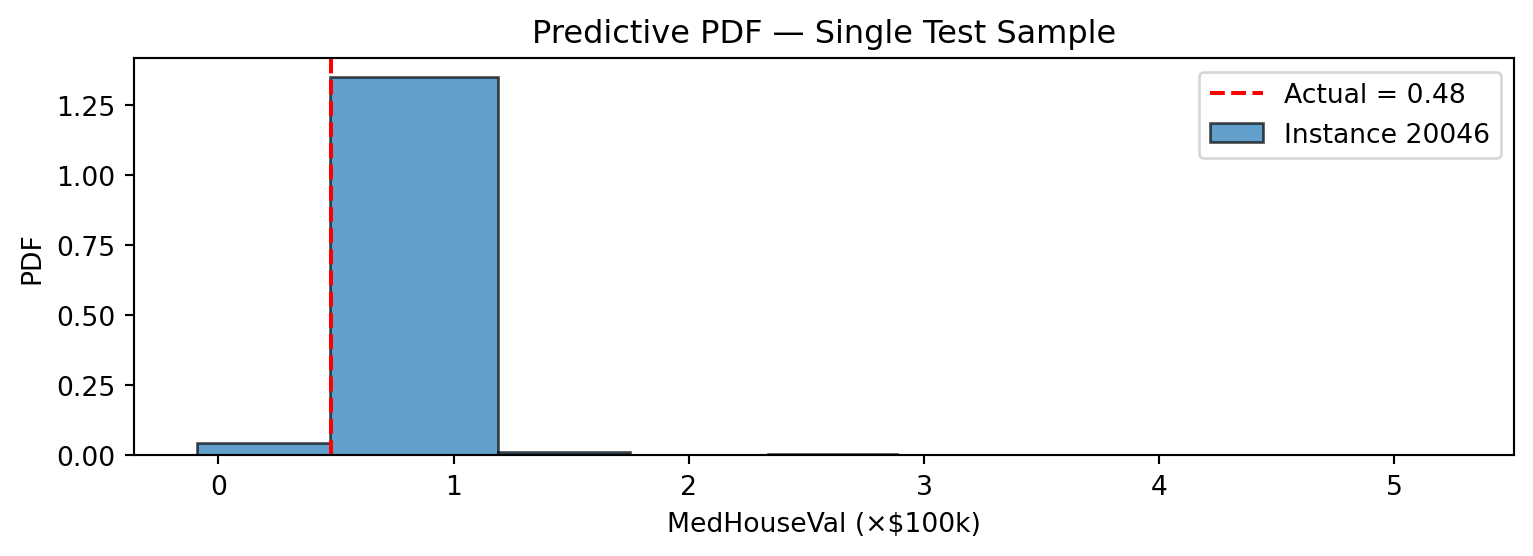

5. Visualizing the Predictive PDF

IntervalDistribution has a built-in plot method that renders the piecewise-constant density as histogram-like bars.

import matplotlib.pyplot as plt

# Single test sample

idx = y_test.index[0]

dist_single = dist.loc[[idx]]

fig, ax = plt.subplots(figsize=(8, 3))

dist_single.plot(ax=ax, alpha=0.7)

ax.axvline(

y_test.loc[idx],

color="red",

linestyle="--",

label=f"Actual = {y_test.loc[idx]:.2f}",

)

ax.set_xlabel("MedHouseVal (×$100k)")

ax.set_ylabel("PDF")

ax.set_title("Predictive PDF — Single Test Sample")

ax.legend()

plt.tight_layout()

plt.show()

# Four samples side by side

fig, axes = plt.subplots(1, 4, figsize=(16, 3))

for ax, i in zip(axes, range(4)):

row_idx = y_test.index[i]

dist.loc[[row_idx]].plot(ax=ax, alpha=0.7)

ax.axvline(y_test.iloc[i], color="red", linestyle="--", linewidth=1.5)

ax.set_title(f"Sample {i}")

ax.set_xlabel("y")

plt.suptitle("Predictive PDFs — PartitionTreeRegressor", y=1.02)

plt.tight_layout()

plt.show()

6. Partition Forest — Better Calibrated Distributions

PartitionForestRegressor averages the conditional densities from multiple trees, producing smoother and better-calibrated distributions.

from partition_tree.skpro import PartitionForestRegressor

pf = PartitionForestRegressor(

n_estimators=50,

random_state=42,

min_volume_fraction=0.1,

output_distribution="mixture",

)

pf.fit(X_train, y_train)

dist_forest = pf.predict_proba(X_test)

y_pred_forest = pf.predict(X_test)7. Random Forest comparison

from sklearn.ensemble import RandomForestRegressor

rf = RandomForestRegressor(

n_estimators=50,

random_state=42,

)

rf.fit(X_train, y_train)

y_pred_rf = rf.predict(X_test)Point metrics comparison

pd.DataFrame({

"Model": ["DecisionTree (CART)", "PartitionTree", "PartitionForest", "RandomForest"],

"RMSE": [

root_mean_squared_error(y_test, y_pred_cart),

root_mean_squared_error(y_test, y_pred_pt),

root_mean_squared_error(y_test, y_pred_forest),

root_mean_squared_error(y_test, y_pred_rf),

],

"R²": [

r2_score(y_test, y_pred_cart),

r2_score(y_test, y_pred_pt),

r2_score(y_test, y_pred_forest),

r2_score(y_test, y_pred_rf),

],

}).round(4)| Model | RMSE | R² | |

|---|---|---|---|

| 0 | DecisionTree (CART) | 0.7037 | 0.6221 |

| 1 | PartitionTree | 0.5879 | 0.7362 |

| 2 | PartitionForest | 0.5076 | 0.8034 |

| 3 | RandomForest | 0.5072 | 0.8037 |

Coverage comparison

lower_f = dist_forest.ppf(0.10)["MedHouseVal"]

upper_f = dist_forest.ppf(0.90)["MedHouseVal"]

covered_f = ((y_true >= lower_f.values) & (y_true <= upper_f.values)).mean()

print(f"Tree 80% PI coverage: {covered:.1%}")

print(f"Forest 80% PI coverage: {covered_f:.1%}")Tree 80% PI coverage: 76.1%

Forest 80% PI coverage: 94.1%output_distribution option

PartitionForestRegressor supports two strategies for combining per-tree distributions:

output_distribution |

Description |

|---|---|

"merged" (default) |

Merges all tree breakpoints into one IntervalDistribution. Full API support, computed once at predict time. |

"mixture" |

Returns a MixtureIntervalDistribution. PDF/CDF/quantiles computed on-the-fly; avoids the merge cost. |

pf_mix = PartitionForestRegressor(

n_estimators=50,

random_state=42,

min_volume_fraction=0.1,

output_distribution="mixture",

)

pf_mix.fit(X_train, y_train)

dist_mix = pf_mix.predict_proba(X_test)8. Feature Importances

Feature importances are accumulated log-loss gain across all splits:

importances = pt.get_feature_importances(normalize=True)

for feat, imp in importances.items():

print(f" {feat:>20s}: {imp:.4f}") target_MedHouseVal: 0.2436

MedInc: 0.1911

Longitude: 0.1513

Latitude: 0.1367

AveOccup: 0.1089

AveRooms: 0.0481

HouseAge: 0.0434

Population: 0.0411

AveBedrms: 0.0358